Using Your 401(k) for a Down Payment, Smart Strategy or Risky Tradeoff?

Buying a home already feels like an endurance sport with unclear rules. Now the federal government may be considering a move that could fundamentally change how buyers get in the game.

According to CNBC, policymakers are exploring whether Americans could withdraw money from their 401(k) retirement accounts to use toward a down payment on a home, potentially without early withdrawal penalties. If implemented, this would be a major shift in how retirement savings and homeownership intersect.

For buyers stuck with solid incomes but insufficient cash, this proposal lands like a flashing yellow light, promising opportunity and warning at the same time.

What the Rules Are Today

Before imagining granite countertops funded by your future self, it helps to understand what is already allowed.

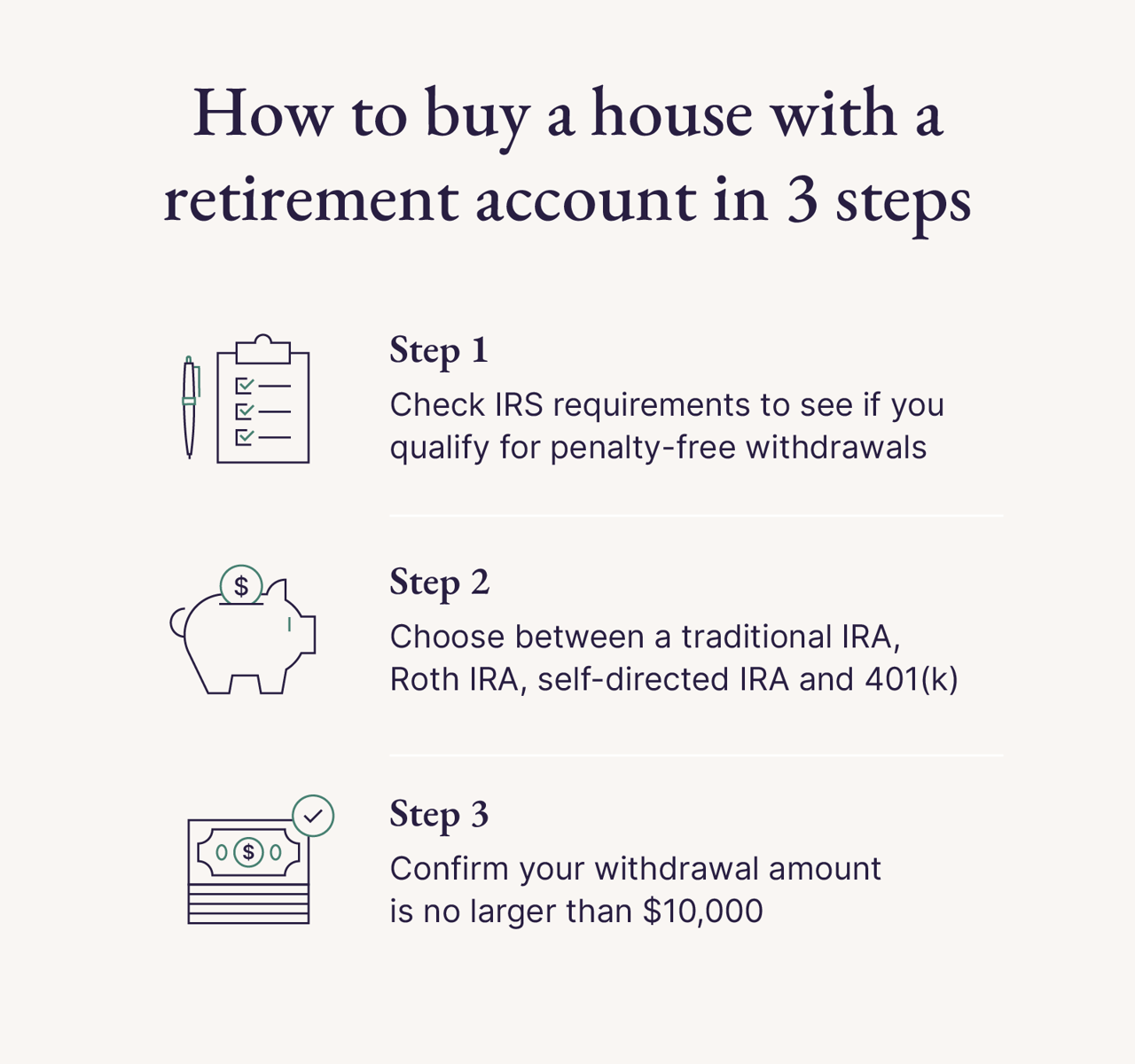

First-time homebuyers who hold Individual Retirement Accounts, or IRAs, can currently withdraw up to $10,000 penalty free to buy, build, or rebuild their first home. Income taxes still apply, but the early withdrawal penalty is waived.

This rule has quietly helped many buyers bridge small but critical gaps in down payments, especially in high cost markets.

401(k)s are different. They are employer sponsored, typically larger, and tightly protected by penalties designed to keep the money untouched until retirement. That is why any change here would be significant.

Why This Is Being Discussed Now

Housing affordability remains strained. Prices are high, rates are higher than buyers want, and saving for a down payment has become the biggest obstacle to ownership, especially for first-time buyers.

Many Americans technically have money, it just lives inside retirement accounts they are not allowed to touch. This proposal acknowledges a mismatch between modern housing markets and outdated financial guardrails.

From a policy standpoint, it is an attempt to expand access to homeownership without rolling out new subsidy programs or tax credits.

Potential Benefits for Buyers

Used conservatively, access to 401(k) funds could help buyers who are already financially responsible but blocked by upfront costs.

-

Larger down payments may reduce monthly mortgage payments

-

Buyers could avoid or reduce private mortgage insurance

-

Some may enter the market sooner, building equity instead of waiting while prices rise

In expensive urban markets, even a modest boost in upfront cash can change the entire affordability equation.

The Risks You Cannot Ignore

This is where enthusiasm needs adult supervision.

Money removed from a 401(k) loses years of compound growth. That growth is what makes retirement math work in the first place. A dollar taken out today is not just a dollar lost, it is decades of missed appreciation.

There is also a behavioral risk. Once retirement accounts are seen as flexible, they may be treated that way, not just for homes but for every urgent or tempting expense that follows.

A home can be a powerful wealth building tool, but it does not replace a retirement plan.

Smart Considerations Before Tapping Retirement Funds

If this policy becomes reality, buyers should approach it strategically, not emotionally.

-

Use retirement funds to improve loan terms, not stretch budgets

-

Withdraw the minimum amount that makes a real difference

-

Run long term projections with a financial advisor

-

Factor in ongoing homeownership costs, not just the purchase

A home should support long term stability, not undermine it.

The Bigger Picture for Homeownership

This proposal reflects a broader shift in how financial security is evolving. The traditional path, save quietly for retirement while renting indefinitely, no longer matches how housing markets operate.

The government appears to be recognizing that blocking access to homeownership has long term economic consequences of its own. Whether this approach proves helpful or harmful will depend entirely on how tightly it is regulated and how thoughtfully buyers use it.

For some, this could be the key that unlocks the front door. For others, it could be a decision they wish they had thought through more carefully.

As with most things in real estate, access creates opportunity. Judgment determines outcomes.If you are a first-time buyer navigating down payment strategies, affordability, or long term planning in today’s market, understanding all your options matters. Smart decisions upfront tend to age better than impulsive ones.