Mortgage rates feel high right now. That sentiment is everywhere. But feelings and facts are not the same thing, and real estate decisions benefit from historical perspective.

Looking at long-term mortgage data, today’s rates are far from unprecedented.

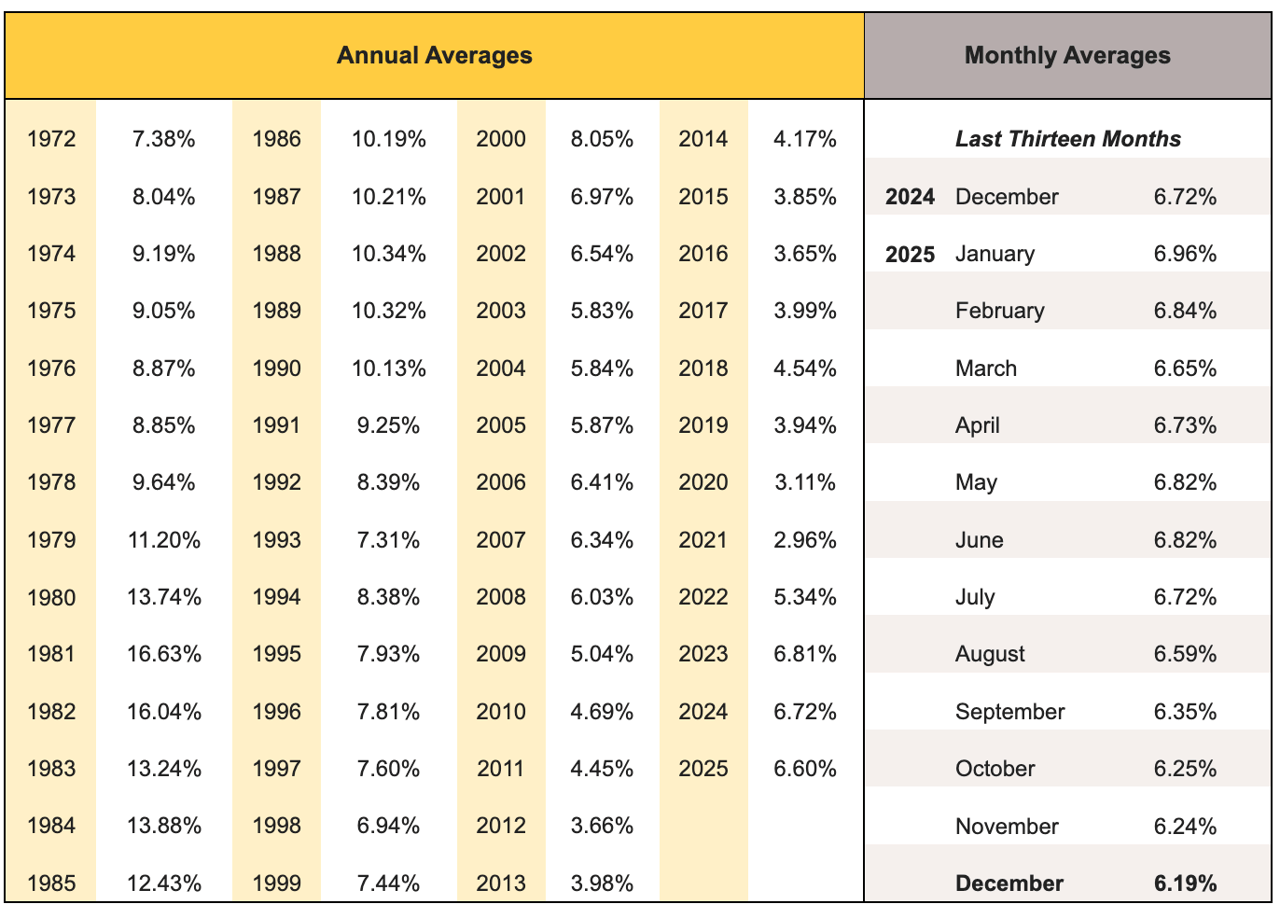

A Look Back at Mortgage Rates Over Time

Mortgage rates have moved in wide cycles for decades. In the late 1970s and early 1980s, average annual mortgage rates regularly exceeded 10%, peaking above 16% in the early 1980s. Buyers still bought homes, not because it was easy, but because housing decisions were tied to life, not perfection.

By contrast:

-

In the early 2000s, rates hovered between 6–8%

-

Following the 2008 financial crisis, rates trended downward

-

Between 2020 and 2021, rates fell below 3%, an extreme historical outlier

Those ultra-low rates distorted buyer expectations. They were never normal, and they were never sustainable.

Where We Are Now

Over the last year, mortgage rates have largely ranged between the mid-6% and high-6% range. Month to month, the fluctuations have been modest, not dramatic.

That puts today’s rates:

-

Well below long-term historical averages

-

Higher than the post-pandemic anomaly

-

Much closer to what previous generations considered normal

The idea that today’s rates are “unaffordable” in isolation ignores decades of data.

Why Context Matters for Buyers

Housing affordability is shaped by more than rates alone. Prices, wages, inventory, taxes, and lifestyle needs all matter. Waiting indefinitely for the “perfect” rate often means sitting out years of potential equity growth, stability, or life progress.

Historically, buyers who focused solely on timing rates often missed opportunities available when they actually had the ability to buy.

The Bigger Picture

Mortgage rates move in cycles. They always have. What changes is how anchored people become to the most recent extreme.

The past few years reset expectations in a way that may take time to unwind. But history suggests that today’s rates are not abnormal, they’re a return to a more typical environment.

Perspective doesn’t make payments smaller, but it does make decisions clearer. If you’re trying to decide whether to buy, wait, refinance, or reassess based on mortgage rates, I can help you evaluate the numbers with context, not noise.